The health insurance mandate, probably the most visible outcome of the Patient Protection & Affordable Care Act (ACA or Obamacare), goes into effect in January. Enrollment in the health insurance exchanges opens October 1, so much attention has been focused on the premiums: Supporters of the law hope for lower rates; opponents have been widely predicting that rates would soar.

The health insurance mandate, probably the most visible outcome of the Patient Protection & Affordable Care Act (ACA or Obamacare), goes into effect in January. Enrollment in the health insurance exchanges opens October 1, so much attention has been focused on the premiums: Supporters of the law hope for lower rates; opponents have been widely predicting that rates would soar.

In July, premiums for New York State’s Health Insurance Marketplace were released and revealed two notable facts: First, premiums in the individual market are far below current rates. Second, Rochester has the lowest rates in the state.

First, the individual market: A central goal of the law has been to get more people covered by health care insurance. In most states, this has been prohibitively expensive for individuals and small groups. Insurance is all about the odds—for any randomly selected group, catastrophic illness ($$$$$!) is rare. When health insurance is optional, the share of buyers who are sick soars and premiums do, too. As premiums go up, more healthy people drop coverage and the premiums ratchet up again. That’s why employer groups can be insured affordably—although these groups aren’t random, neither is the “pool” biased in favor of people with health problems.

The Urban Institute reported last year that the monthly premium for an individual plan in New York was nearly $1,300. Apparently only about 32,000 people out of 14 million insured New Yorkers needed coverage badly enough to pay so much. Most analysts believe that the high rates (and consequent low enrollment) could be explained by a New York law requiring that insurers to accept all applicants regardless of condition (called “guaranteed issue” in wonkland). As coverage wasn’t required, the “pool” of buyers was small and premiums became unaffordable.

Guaranteed issue is also part of the ACA legislation. But so is a coverage mandate: As of January, you must either jump in the pool or pay a fine. So the big question remains: What will happen to rates? In New York State’s individual market, rates will fall significantly. The state recently released approved rates for New York’s Health Insurance Marketplace (the “exchange”). And the monthly premium for individual plans came under $600—that’s for the “gold” plan averaged across all regions and providers.

New York law is like the Affordable Care Act in two other respects: New York has long required a base level of coverage, and has required insurers to charge small groups a rate based communitywide costs, not the health cost experience of the group (called “community rating”—See economist Uwe Reinhardt’s discussion here). States without guaranteed issue, a base level of coverage or community rating will probably see insurance rates rise under ACA.

See additional discussion of the NYS rates in this Washington Post story and further analysis of the NYS market under ACA in this Deloitte study.

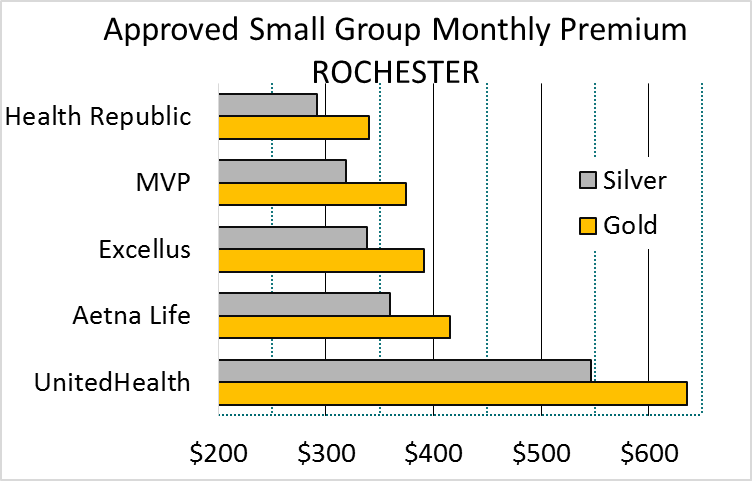

How about the small group market? With community rating and minimum coverage already in place, the premiums approved by NYS seem roughly in line with current pricing. Here in Rochester, five insurers have approved rates for “gold” and “silver” plans (only three submitted “platinum” and “bronze” plans).

How about the small group market? With community rating and minimum coverage already in place, the premiums approved by NYS seem roughly in line with current pricing. Here in Rochester, five insurers have approved rates for “gold” and “silver” plans (only three submitted “platinum” and “bronze” plans).

Time out for more ACA jargon: These “metal” tiers refer to the “actuarial value” of the plans. The highest level of coverage is the platinum plan—you pay the highest premium, but the plan is designed to cover about 90% of the cost of care, on average. Consumers in these plans will collectively pay about 10% of the total. The gold plans are designed to insure the consumer against 80% of the cost; silver pays 70%; and bronze plans pay 60% of the cost.

Back to the rates: The monthly premium for Rochester’s gold plans ranges from $340 from Health Republic to $636 from UnitedHealth. The silver plans are 14% cheaper on average. A silver plan from MVP or Excellus will cost between $3,800 and $4,000 per year.

Few of us are average, of course. We’ll still have to pick the plan that fits our circumstance. Someone who is young and healthy may choose a bronze plan, save about $800 on the premium and hope to need little care. Or you may hate co-payments and deductibles and are willing to pay more upfront to avoid them.

A note about Health Republic: This is a new insurer started as a co-op with the help of the Freelancers Union of New York City. If you sign up, you’ll receive care through MagnaCare, a network that reports 70,000 providers in New York and New Jersey. Its website listed more than 200 primary care physicians in the Rochester area.

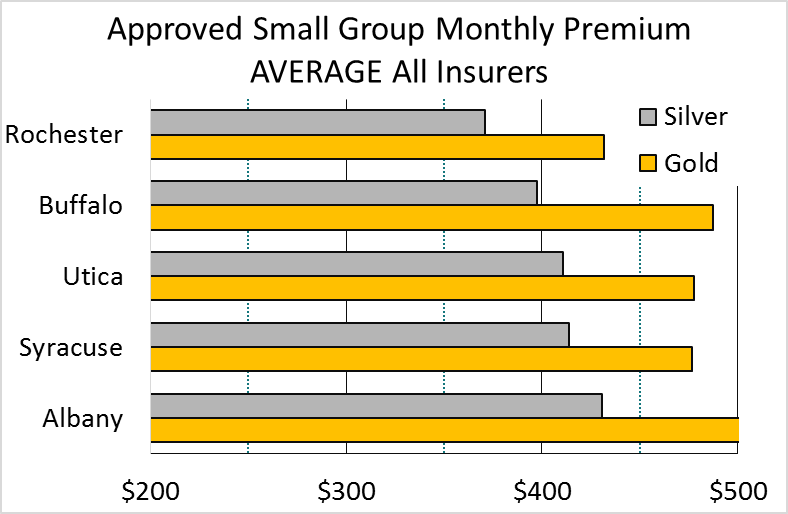

Finally, Rochester posts lowest premiums: One by-product of the Health Insurance Marketplace is the publication of rates from different parts of the state. We’ve long heard that the “Rochester model” keeps health care costs down. Apparently the insurers believe this to be true as Rochester has the lowest approved premiums in the state—about 14% below the average for the remaining regions (less NYC) for the gold plans.

Finally, Rochester posts lowest premiums: One by-product of the Health Insurance Marketplace is the publication of rates from different parts of the state. We’ve long heard that the “Rochester model” keeps health care costs down. Apparently the insurers believe this to be true as Rochester has the lowest approved premiums in the state—about 14% below the average for the remaining regions (less NYC) for the gold plans.

That’s the news from the NYS rollout of the Affordable Care Act. We’ll watch with interest (and some apprehension) as this tremendously complex legislation is implemented.