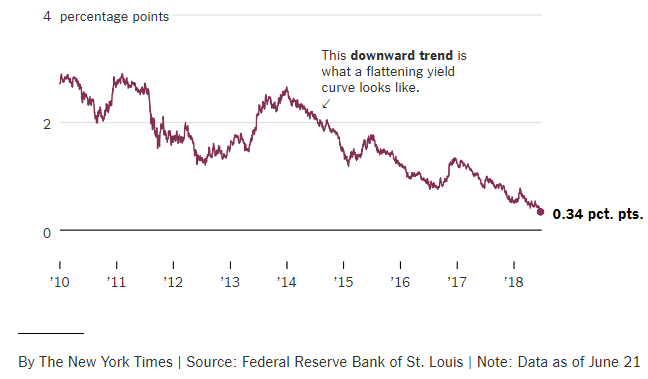

The yield curve compares interest rates charged on long term and short term bonds—typically, 10 year v. 2 year U.S. Government treasuries. When the 10 year rate is lower than the 2 year rate, the yield curve is said to be “inverted” and may be “predicting” a recession.

The yield curve is nothing but a sophisticated investor confidence survey—if investors expect inflation will rise, then they will demand a higher yield (or interest rate) for longer maturity bonds.

Some of you may remember the TV series, Early Edition. Every morning the protagonist found tomorrow’s newspaper outside his door. Blessed (or cursed) by knowledge of the future, he spent the rest of the episode trying to fix things.

Suppose you found the Wall Street Journal from 2028 on your doorstep or in your email’s inbox and learned that inflation, 2% today, had risen steadily to 5%. To compensate for the loss in inflation-adjusted yield (the interest rate minus inflation), you would demand a higher interest rate for bonds with longer maturities.

On the flip side, if your “early edition” of the WSJ showed inflation to have stayed the same or fallen, you’d be willing to accept a lower yield (rate of interest). Read more »

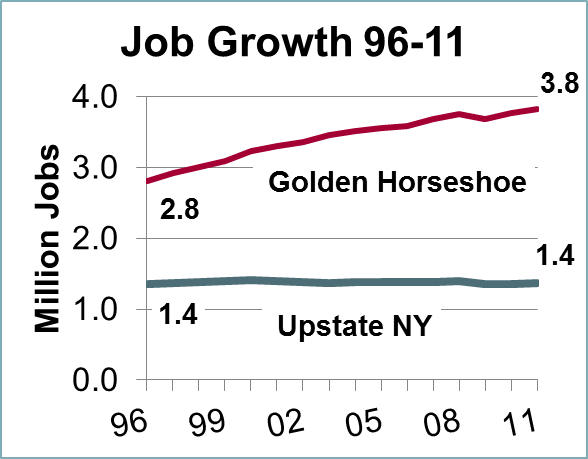

Remember the Fast Ferry connecting Rochester and Toronto? Although the idea failed in execution, connecting with the vibrant “Golden Horseshoe” economy made sense then—and still does today. When we compare Rochester to, say, Charlotte or Atlanta or Austin, we can always blame the snow. But that doesn’t work when we look across the lake. What’s their “secret sauce?”

We may be separated only by a bit of water and a line on a map, but it is clear that Canada’s Golden Horseshoe Region, powered by Toronto, has prospered while Upstate New York (defined here as Rochester, Buffalo and Syracuse) has just held its own. Although these neighboring regions share much—that climate, access to markets, and transportation infrastructure—since 1996 the Golden Horseshoe added more than a third to its employment base and a quarter to its population. Read more »

I love summer and I love sports. 2012 has already produced many sports highlights with I’ll Have Another winning 2/3 of horse racing’s Triple Crown, Tiger Woods’ renewed success on the golf tour, Roger Federer’s and Serena Williams’ record breaking tennis wins at Wimbledon, the mid-summer classic, baseball’s All-Star game and King James winning his first NBA title. And now it’s the Tour de France and, soon, the summer Olympic Games.

Big Sports Event = Big Economic Impact?

Sports spectaculars are often lauded for their economic impact. Does the reality match the claims? Victor Matheson, an economics professor at College of the Holy Cross in Massachusetts has analyzed the economic impact of “mega sporting events” like the Super Bowl, the Olympics, the All Star Game, and World Series. He finds many examples of major sporting events not living up to their pre-event hype. For instance, Major League Baseball claims economic impact on cities that host the All-Star game in the neighborhood of $75 million in direct benefits. Matheson’s ex post research suggests that for the cities that hosted All-Star games between 1973–1997, average employment actually declined by a half percent. Organizers of the 1996 summer Olympics in Atlanta suggested upwards of 77,000 new jobs would be generated. Matheson estimates that as few as 3,500 were actually created. Read more »

Given a conflict between “good for us” or “good for me,” people generally pick the second. That proposition, obvious as it is, underlies most of economics. Thank goodness, human beings often rise above self-interest in ways that redeem human society.

But politicians shouldn’t push their luck. Consider what the European Union is asking of the Greeks. The austerity imposed as a condition of the bailout goes beyond expecting Greeks to behave like Germans, which would be heroic enough. No, the Greeks are expected to do penance for their past profligacy, the “sackcloth and ashes” Full Monty.

Kidding ourselves

Reluctant to think ourselves selfish, we have a remarkable capacity to convince ourselves that “good for me” is also “good for us.” That capacity for self-delusion is evident in results from the Pew Global Survey: Respondents in Britain, France, Germany, Greece, Spain, Italy, Poland and the Czech Republic were asked to identify the “hardest working” people of Europe. Seven picked the Germans. The Greeks picked themselves. For the title, “least hardworking,” five picked the Greeks, but the Greeks fingered the Italians.

Is it any wonder that the Greeks’ penance is insincere? Or that support for austerity among voters proved to be so tenuous in Sunday’s election? Read more »

I remember the looks on the faces of my undergrad sociology classmates when they learned I was also majoring in business. A traitor was in the ranks! How could I possibly be one of the good guys while learning about global markets? Conversely, in my business courses I was suspect for having an affinity for the “softer” side of academia—subjects that surely weren’t as important or rigorous as microeconomics.

This stereotyping divided our student body – groups were aware of each other, but rarely interacted and certainly didn’t recognize their commonalities in perspective or purpose. During my professional career I have witnessed similar antics between our sectors – nonprofit, business, and public. Sure, we know the others exist, but we aren’t really playing on the same team. Read more »

“And which retirement plan do you want?” Retirement?!! As a newly appointed Assistant Professor of Economics at Potsdam College of SUNY, I was 28 and starting my first real professional job. I was being asked to make a decision that would have little impact on my life for 37 years.

I was offered two options: The first was the NYS Employee Retirement System (ERS). If I stayed in state service and retired at age 65, I would be eligible for annual benefits equal to 70.5% of my final average salary (defined as the highest salary earned in three consecutive years). My contribution would have been 3% of salary for the first ten years. The remainder of the cost would be paid by the state. This is what is called a “defined benefit” retirement plan. Regardless of what happens to the invested money, NYS promises to pay out a specified benefit for as long as I live. Read more »

Congress is edging closer to passing legislation that restructures health insurance. The Senate and the House are debating compromise bills within their houses, after which a conference committee will seek to reconcile differences between them. With these details still under debate, we conclude our six part series on health reform with a few observations.

Public Option. If private insurance plans are part of the problem, then one solution may be to offer another option, a health insurance plan that is run by the government. At this writing, a “public option” seems likely to survive and become part of the final legislation. The debate over the public option has highlighted a fundamental social tension between those who fear too much government and those who fear too little (discussed in the first column in this series). Like Goldilocks, each of us wants the balance to be “just right.”

In this column, we address the challenge of expanding health insurance coverage. First, we explore why our employer-based system leaves gaps in coverage, even for people with jobs. Second, we discuss the challenge of relying on the individual insurance market, which has to fill these gaps.

Remember “mutual assured destruction?” MAD was the dominant principle of the Cold War: The Soviet Union would not attack us as long as we retained the ability to retaliate. They might surprise us and obliterate New York, Chicago, Los Angeles, and Washington, but our nuclear subs and hardened silo-based missiles would respond in kind, turning Moscow, Leningrad, Kiev and Vladivostok into historical footnotes (if mankind survived to write any more history).

A kind of financial “MAD” became our consolation in the 1990s as China continued to accumulate foreign exchange, the vast majority of which was in dollars (or financial assets like bonds that were priced in dollars). At present, China’s holdings of dollar assets top $1.5 trillion, says the Peterson Institute for International Economics.

I’ve been in a funk since the 2009-10 state budget passed. The state’s elected leaders entered the budget negotiations confronting a potential $20 billion deficit, up from the $14 billion estimated when the Governor released his original budget proposal. That is, the state would have run a $20 billion deficit in 2009-10 if spending and revenue continued without changing anything structural (like tax rates or spending formulae). The faltering economy could no longer satisfy the state’s addiction to ever-greater spending.

Given such a dire forecast, we all wondered how the state would manage to find the money to avoid a major reduction in spending. Imagine our surprise when the Legislature and Governor pulled a rabbit out of the budgetary hat and increased budgeted spending by $12 billion, nearly 9% more than in 2008-09.

The yield curve compares interest rates charged on long term and short term bonds—typically, 10 year v. 2 year U.S. Government treasuries. When the 10 year rate is lower than the 2 year rate, the yield curve is said to be “inverted” and may be “predicting” a recession.

The yield curve compares interest rates charged on long term and short term bonds—typically, 10 year v. 2 year U.S. Government treasuries. When the 10 year rate is lower than the 2 year rate, the yield curve is said to be “inverted” and may be “predicting” a recession.

I love summer and I love sports. 2012 has already produced many sports highlights with I’ll Have Another winning 2/3 of horse racing’s Triple Crown, Tiger Woods’ renewed success on the golf tour, Roger Federer’s and Serena Williams’ record breaking tennis wins at Wimbledon, the mid-summer classic, baseball’s All-Star game and King James winning his first NBA title. And now it’s the Tour de France and, soon, the summer Olympic Games.

I love summer and I love sports. 2012 has already produced many sports highlights with I’ll Have Another winning 2/3 of horse racing’s Triple Crown, Tiger Woods’ renewed success on the golf tour, Roger Federer’s and Serena Williams’ record breaking tennis wins at Wimbledon, the mid-summer classic, baseball’s All-Star game and King James winning his first NBA title. And now it’s the Tour de France and, soon, the summer Olympic Games.